POTENTIAL LOSSES FROM FOSSIL FUEL INVESTMENTS

Analysis by Truzaar Dordi, University of Waterloo

The University of Waterloo has potentially lost upwards of $20 million between 2011 and 2015 through its investments in fossil fuels. This result is not surprising, many investors suffered similar loses. Corporate Knight’s decarbonizer tool finds trillions in lost opportunity. Most noteworthy may be the Bill and Melinda Gates Foundation, which after rejecting calls to divest from fossil fuels, lost $1.9 billion between 2012 and 2015.

Some may argue that the University should maintain its its fossil fuel investments lest it lose out. However, the opposite concern – that keeping these investments is financially risky – may be the greater concern. The well-recognized terminal decline of the coal industry shows that not every bust is followed by a new boom once clean energy technologies mature.

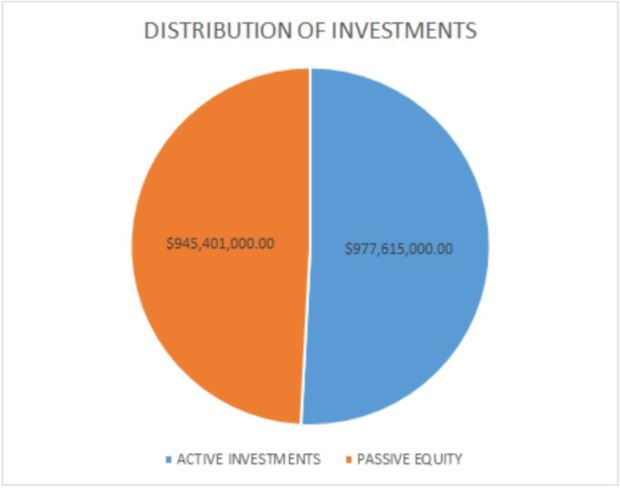

We know that the University of Waterloo holds investments in the form of pensions, endowments, and trusts, that are distributed equally between active investments and passive equities (Appendix). While there is information on the CU200 exposure of the active holdings, the CU200 exposure of passive funds is unknown. With this, we can approximate the losses the university may have realized through their fossil fuel holdings.

The University of Waterloo has a total of $1,923,016,000 of pensions, endowments and trusts. Approximately $945,401,000 are invested in passive equity funds, the remaining of which are in active investments.

Companies listed on the Carbon Underground 200 encompass 3.56% of active holdings. The distribution of Carbon Underground 200 companies in passive funds are unknown. Exposure for passive funds may be the same as active investments (at 3.56%) however, this is not indicated. Alternatively, the MSCI world index has 8.3% exposure, Canadian equities have an average exposure of 19.5%, and the TSX composite has an exposure of 22.6%. Without clear indication of passive holdings, investments in the Carbon Underground 200 may be anywhere between $68,495,000 (3.56% of total investments) and $248,464,000 (12.9% of total investments).

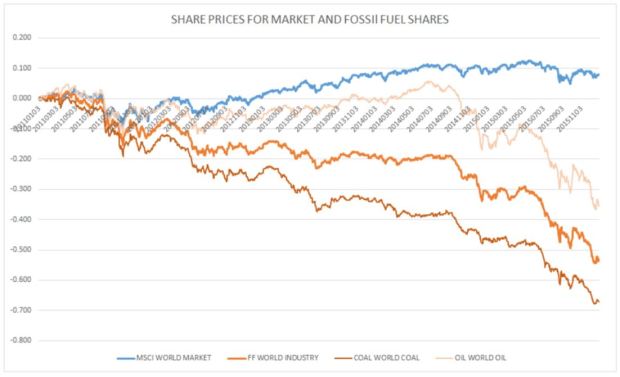

Using financial data for the Carbon Underground 200 and the MSCI all country world index, we can predict approximately how much the university may have lost in recent years. We use data over the period of January 2011 to December 2015 (5 years). The data indicates that the MSCI market proxy increased by about 7.8% over the course of the time frame, whereas the Carbon Underground 200 fell by about 53.6%. The drop in share prices was more prominent for the Coal 100 (-67.1%) than the the Oil and Gas 100 (-35.5%).

Assuming the University of Waterloo held a total of $1,923,016,000 in the beginning of 2011, we can measure how much the university may have gained and lost over the following years. The table below provides a preliminary measure of how investments may have performed relative to a portfolio with no Carbon Underground investments. One important result from this is that even if passive equities are not invested in the Carbon Underground 200, the University would have realized a 14% loss ($21,000,000) from their direct exposure in active investments, relative to a fossil free portfolio, between 2011 and 2015.

The financial case for divestment is simply an exercise to demonstrate the implications of climate change for financial markets. The effects of climate change will be pervasive, depreciating more than just fossil fuel investments. To take a prudent approach to financing, we advocate for improved metrics beyond mandated requirements, that take a broader approach to managing climate risks. In doing so, the University will be better equipped to manage the financial impacts of climate change.